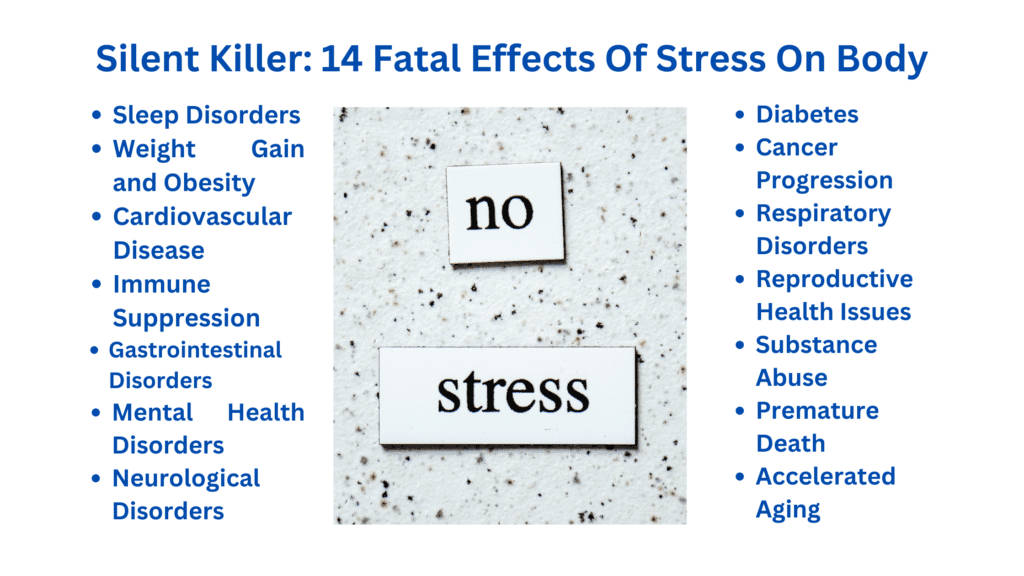

Debt stress in marriage is not limited to numbers, repayments, or financial calculations; it gradually becomes a psychological and relational burden that affects how couples think, communicate, and make decisions together. When credit card debt problems enter a relationship—especially through hidden actions or lack of transparency—they often trigger deeper issues such as loss of trust, emotional distance, and constant anxiety.

Over time, even stable households begin dealing with financial stress in ways that impact their daily functioning. This is where debt and mental health become closely connected, as uncertainty and fear begin to dominate conversations. Understanding how to get out of debt is not just about repayment strategies; it also requires emotional clarity, accountability, and a structured debt repayment plan that considers both financial reality and relationship stability.

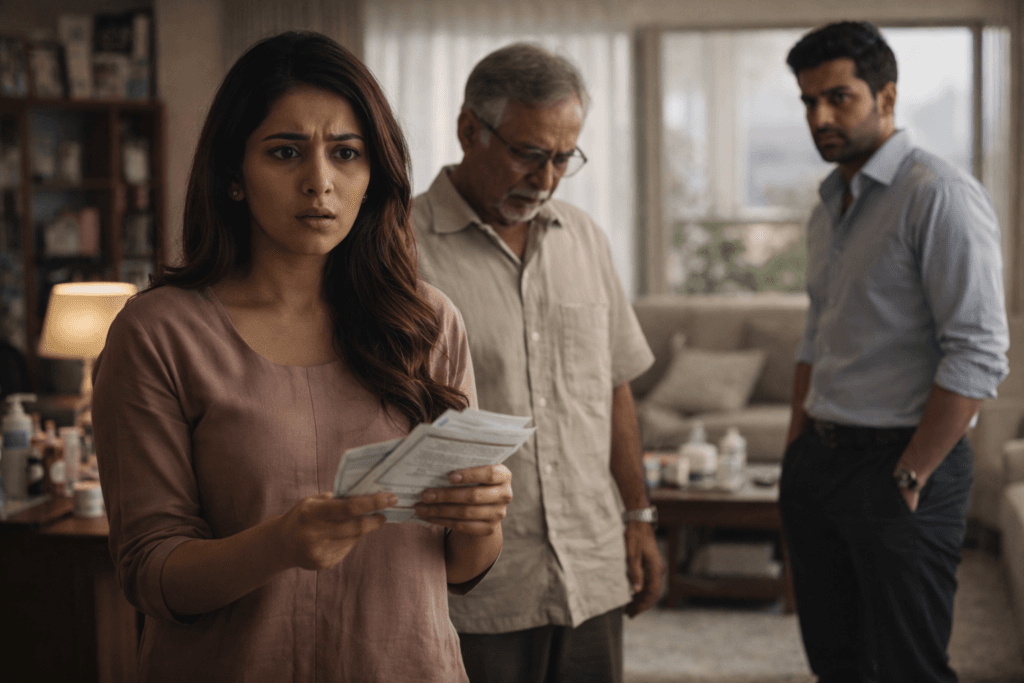

Nidhi (name changed) never thought her beloved husband would put her under 30 Lacs debt. In her case, the situation clearly shows how financial stress in marriage can escalate when trust is replaced by blind dependence. What initially appeared to be a supportive and stable family setup slowly turned into a severe crisis when her husband accumulated a 30-lakh liability through 20+ credit cards. Her husband even forged their signatures to accumulate those credit cards. This is not just an example of managing credit card debt gone wrong, but a deeper issue involving financial problems in a relationship and rising family financial problems.

When confronted, her husband threatened them that he would create a scene in front of her ailing mother if they kept hammering him. In short, Nidhi’s husband simply instructs her to resolve the crisis silently without making it an issue. The pressure is not only about repayment but also about protecting her ailing mother and emotionally affected father while navigating manipulation. This level of debt stress highlights the importance of early awareness, structured financial boundaries, and practical debt management tips to prevent such situations from becoming overwhelming.

Table of Contents

ToggleFinancial Stress in Marriage: When Debt Becomes a Relationship Crisis

Financial stress in marriage often begins subtly, through small financial decisions, temporary income disruptions, or risk-taking driven by optimism. However, when these decisions are made without transparency or accountability, they can evolve into serious relationship conflicts.

Dealing with financial stress requires consistent communication, shared decision-making, and clearly defined boundaries to ensure that both partners remain aware of financial realities. Without these structures, even financially stable households can experience rising debt stress, leading to emotional strain and mistrust. Over time, unresolved issues can transform into deeper financial problems in a relationship, where money becomes a source of tension rather than stability.

In Nidhi’s case, the family initially had no significant financial burden. Nidhi’s father was earning a handsome income, Nidhi is a working professional, and her mother was getting their rental income. But the situation changed when her husband gained unchecked control over the financial matters of the entire household. He would handle the bank and lockers as well. Nidhi and her parents blindly trusted him and handed him over the banking responsibility. His actions, including taking multiple credit cards with forged signatures, then misusing them, and hiding liabilities, pushed the household into severe debt stress.

This reflects how financial stress in marriage can escalate rapidly when oversight is absent. The challenge now extends beyond repayment, involving rebuilding trust, addressing manipulation, and managing growing family financial problems with clarity and control. Many times, families simply can’t recover those trust issues, and it leaves permanent damage to the relationship dynamic.

Family Financial Problems and Emotional Pressure

Family financial problems rarely remain confined to numbers; they extend into emotional spaces, creating pressure, fear, and internal conflict within the household. When one individual’s financial decisions affect everyone, the emotional burden becomes collective, even if responsibility is uneven. This is where debt and mental health begin to overlap, as financial uncertainty starts influencing emotional well-being. Families often try to maintain peace by avoiding confrontation, but this silence can intensify long-term debt stress and complicate dealing with financial stress effectively.

In Nidhi’s situation, the emotional weight is visible in her father’s distress and helplessness after discovering the 30-lakh liability. Since her father was already under huge pressure due to her mother’s health condition. The pressure increases further because her husband is using her mother’s fragile health as leverage, adding psychological strain to existing family financial problems. This demonstrates how health and financial crises can turn into emotional control mechanisms. Instead of resolving the issue, fear is used to delay action, which deepens both financial and emotional instability. He knows forging signatures is a criminal offence, and if his wife takes any action against him, then he will be in real trouble.

Debt Management Tips for Couples

Effective debt management tips for couples focus on transparency, shared responsibility, and regular financial review. Both partners should have equal visibility into financial accounts, liabilities, and spending patterns to prevent misunderstandings or misuse. Establishing spending limits and maintaining documentation for financial decisions can reduce the risk of hidden debt. These practices are essential for dealing with financial stress and maintaining stability within a relationship.

Nidhi’s case clearly shows the consequences of giving one partner unchecked financial authority. The absence of oversight allowed credit card debt problems to grow unnoticed, leading to severe debt stress. Moving forward, strict financial boundaries are necessary, including shared access to accounts and periodic reviews. Applying these debt management tips can help rebuild trust and reduce financial problems in a relationship, ensuring that similar situations do not occur again.

Debt and Mental Health

Debt stress has a direct and often underestimated impact on mental health, leading to anxiety, restlessness, overthinking, and emotional exhaustion. When debt arises unexpectedly or through betrayal, the psychological impact becomes more intense. Individuals often feel trapped between financial obligations and emotional ties, making decision-making difficult. The connection between debt and mental health becomes stronger as uncertainty increases, affecting clarity and confidence in handling the situation.

For Nidhi, the struggle is not limited to understanding how to pay off credit card debt, but also processing how trust was broken within her marriage. She was also clueless about the next course of action now. This internal conflict delays action and increases debt stress, as emotional confusion interferes with practical steps. Ignoring the situation to maintain temporary peace may seem easier, but it often worsens long-term outcomes. Recognizing that dealing with financial stress involves both emotional and financial awareness is essential for regaining control and moving forward.

Credit Card Debt Problems and Their Impact on Families

Credit card debt problems can escalate quickly due to their accessibility and high-interest structures. Without proper monitoring, multiple credit lines can accumulate into a significant financial burden. Families often underestimate how rapidly this type of debt grows, especially when spending is not tracked. This makes managing credit card debt a critical responsibility that requires discipline, awareness, and shared oversight to prevent long-term damage.

In Nidhi’s case, the misuse of more than 20+ credit cards across multiple identities. Precisely speaking, he took a few credit cards in his own name, a few in Nidhi’s name, and a few in Nidhi’s parents’ name. Nidhi’s mother is mostly bedridden, so he forged her signature. Not only that, he forged her and her father’s signatures as well.

This highlights a severe breach of trust and breakdown of financial control. The family remained unaware until the debt reached an unmanageable level, intensifying overall debt stress. This situation reflects how unchecked financial authority can lead to serious family financial problems. It emphasizes the importance of structured monitoring and transparency to ensure that credit card debt problems do not spiral into a crisis.

Managing Credit Card Debt in Marriage

Managing credit card debt in marriage requires a collaborative approach where both partners actively participate in financial decisions. Transparency in accounts, spending patterns, and liabilities is essential to prevent misunderstandings and misuse. Regular financial discussions and reviews help in maintaining clarity and reducing the risk of hidden debt. Effective management of credit card debt involves not only repayment strategies but also preventive measures that ensure long-term stability. Both spouses need to understand that credit card debt is a high-interest loan.

In Nidhi’s situation, the absence of shared oversight allowed her husband to operate independently, leading to severe consequences. Once trust is compromised at this level, rebuilding control becomes necessary through stricter systems and accountability. This includes reviewing all accounts, limiting access, and seeking institutional support where required. Managing such credit card debt problems is not only about clearing dues but also about restructuring financial control to avoid recurrence.

How Overspending Creates Financial Instability

Overspending often goes beyond lifestyle choices and reflects deeper behavioral patterns such as impulsive decision-making or unrealistic expectations. When expenses are consistently funded through credit without a structured debt repayment plan, it leads to long-term instability. Over time, this creates a cycle where borrowing replaces planning, increasing overall debt stress and weakening financial security.

In Nidhi’s case, her husband left his job to start his business. His initial business ambitions were supported by the family with open arms. But the absence of structured planning led to uncontrolled borrowing. This gradually turned into a serious financial crisis, highlighting how financial problems in a relationship can emerge even from well-intentioned decisions.

Nidhi is clueless about where her husband spent such a huge amount! She overlooked the very nature of the credit cards’ interest system. Which is compound interest. It can spiral up pretty easily if unchecked. Without discipline and accountability, overspending can destabilize even financially secure households, making dealing with financial stress more complex and emotionally draining.

How to Pay Off Credit Card Debt

Understanding how to pay off credit card debt begins with complete clarity about the situation, including total outstanding amounts, applicable interest rates, and the legal responsibility attached to each liability. Without this clarity, any attempt at repayment becomes unstructured and ineffective. A well-defined debt repayment plan helps prioritize high-interest liabilities, reduce penalties, and gradually stabilize finances.

This approach also supports dealing with financial stress by replacing uncertainty with a clear direction. Addressing credit card debt problems requires both financial discipline and awareness of possible legal implications, especially when multiple accounts are involved.

In Nidhi’s case, repayment alone is not sufficient because forged signatures introduce legal complexity. This transforms the situation from simple debt stress into a combination of financial and legal concerns. Her family must integrate structured repayment with professional guidance to address fraudulent liabilities. A combined approach—covering both repayment and dispute—can reduce long-term pressure while managing family financial problems effectively.

Debt Repayment Plan for Families

A debt repayment plan for families must be realistic, structured, and aligned with available income and essential expenses. It should prioritize high-interest liabilities while ensuring that daily financial needs remain stable. Consistency and discipline are key to making progress without increasing overall debt stress. Avoiding new liabilities and tracking repayment regularly are essential elements of effective planning, especially when dealing with large or complex obligations.

In Nidhi’s situation, the first step is separating legitimate debt from fraudulent transactions caused by forged signatures. Her case is a legal crisis primarily. Since her mother is mostly bedridden, her actual signature is very much distinguished. She and her father can choose to repay the debt silently with legal help. It will be a huge financial burden on her family. On the other hand, she can take legal steps against her husband, and then her family will be on a much stronger platform.

This distinction is crucial before implementing any debt repayment plan. Once clarity is established, the family can decide their next course of action. This structured approach not only helps in managing credit card debt but also restores a sense of control over growing family financial problems, making the situation more manageable over time. They need a professional’s assistance. Otherwise, in the long term, they will be in a huge financial burden, and it will negatively affect their debt record.

How to Get Out of Debt When Income Is Limited

Understanding how to get out of debt with limited income requires careful prioritization, disciplined spending, and strategic decision-making. It often involves restructuring existing liabilities, negotiating repayment terms, and seeking external guidance where necessary. A structured approach helps reduce debt stress while maintaining essential financial stability. Dealing with financial stress in such situations requires focusing on sustainable solutions rather than temporary adjustments.

In Nidhi’s case, the family has stable income sources, but they were not prepared for a sudden high debt burden. This makes it necessary to explore structured solutions rather than relying on informal methods. Addressing family financial problems at this scale requires a combination of financial planning and legal clarity. Understanding how to get out of debt in such circumstances involves balancing repayment, dispute resolution, and long-term financial protection.

Debt Relief Options

Debt relief options provide structured ways to reduce financial burden, including loan restructuring, negotiated settlements, and legal disputes over fraudulent liabilities. The suitability of each option depends on the nature of the debt and available documentation. These options are particularly important when credit card debt problems involve high interest or legal complications.

In Nidhi’s situation, forged signatures create a strong basis for legal action, which may reduce or eliminate certain liabilities. This makes exploring debt relief options essential for minimizing overall debt stress. Instead of treating all liabilities as valid, the family must carefully assess which debts are enforceable. This approach not only supports managing credit card debt but also reduces the long-term impact of family financial problems. All they have to do is take a pragmatic decision as a family instead of an emotional decision.

Long-Term Financial Stability Planning

Long-term financial stability requires building systems that prevent future crises, including budgeting, controlled financial access, and regular monitoring of accounts. These systems help reduce debt stress by ensuring that financial decisions are transparent and accountable. Sustainable planning also supports dealing with financial stress by creating predictability and reducing uncertainty.

For Nidhi, resolving the current issue is only part of the solution. The family must also ensure that similar financial problems in a relationship do not arise again. It means she needs to decide whether she accepts that huge debt repayment or takes legal steps against her husband. This involves hiring a legal professional who would save her and her family from this financial mess to ensure long-term stability. They can move beyond immediate credit card debt problems and build a secure financial environment with the right decision.

How A Family Can Handle Financial Problems in a Relationship

Handling financial problems in a relationship requires honesty, structured communication, and mutual accountability. Avoiding conflict may provide temporary relief, but it often increases long-term debt stress and emotional strain. Every family must address issues directly, ensuring that financial decisions are shared and documented. If there is one person within the family who is misusing funds and everyone’s income, the family must address it immediately. This approach is essential for dealing with financial stress and maintaining stability.

Another very important step is constant monitoring of the accounts, especially joint accounts. Even if one person is handling everything, the rest of the family should constantly monitor everything. The rest of the family members must check the movement of funds within accounts. Regular checking keeps issues in order, and any normal person would not question that activity.

In Nidhi’s case, silence and blind trust allowed the problem to grow into a serious crisis. Addressing it now requires firm and practical action rather than emotional avoidance. This means even deciding relationship dynamics with the husband. The rest of the family has to prioritize financial safety and accountability of the family. By focusing on transparency and control, couples can manage family financial problems effectively and prevent further escalation.

Key Takeaways for the Debt Crisis in Marriage

Debt stress in marriage extends beyond financial pressure and reflects deeper issues of trust, control, and emotional safety within a relationship. When financial decisions lack transparency, even stable families can face severe disruption. In Nidhi’s case, blind trust and lack of oversight allowed credit card debt problems to grow into a major crisis involving forged signatures and hidden liabilities. This highlights how financial stress in marriage can escalate quickly when accountability is missing.

- Debt stress is not only financial; it directly impacts emotional stability and trust in relationships.

- Credit card debt problems can escalate rapidly when access and monitoring are not controlled.

- Financial stress in marriage increases when one partner has unchecked authority over money.

- Family financial problems often create emotional pressure, especially when vulnerable members are involved.

- Dealing with financial stress requires structured planning, transparency, and shared responsibility.

- A clear debt repayment plan helps reduce uncertainty and provides direction during crises.

- Debt and mental health are closely connected, making emotional clarity essential for decision-making.

- Managing credit card debt requires strict monitoring, documentation, and financial discipline.

- Debt relief options, including legal action in cases like Nidhi’s, can reduce overall financial burden.

- Understanding how to get out of debt involves both financial strategy and emotional awareness.

Frequently Asked Questions

How to pay off credit card debt quickly?

Ans. Paying off credit card debt quickly requires a structured approach that begins with identifying all liabilities, interest rates, and repayment priorities. A focused debt repayment plan should target high-interest balances first while maintaining minimum payments on others.

In situations like Nidhi’s, where credit card debt problems involve serious legal complexity, their approach should be way more practical. Here, the first issue is establishing legal clarity, and then the liability needs to be measured. This approach reduces debt stress while improving financial control.

How to get out of debt when it feels overwhelming?

Ans. Understanding how to get out of debt starts with breaking the situation into manageable steps. Assess liabilities, separate valid obligations from disputed ones, and build a realistic plan. Assess the present financial burden, and then decide how to repay in small parts.

For Nidhi’s family, addressing both repayment and legal aspects is necessary because the amount is huge. Dealing with financial stress requires emotional clarity, along with financial planning, to ensure decisions are not driven by fear or confusion. Nidhi’s family has to take legal action to address the issue.

How does debt stress affect relationships?

Ans. Debt stress affects relationships by creating mistrust, emotional strain, and communication breakdown. Hidden decisions or misuse of finances often lead to serious financial problems in a relationship. Often leads to a long-term financial burden that can affect families’ well-being.

In Nidhi’s case, the issue is not just the debt but the breach of trust and manipulation. This shows how debt and mental health are interconnected, influencing both emotional well-being and relationship stability.

What should couples do when facing financial problems in a relationship?

Ans. Firstly, one should not expect blind faith from the significant others. There should be regular monitoring of accounts. Couples should focus on transparency, shared decision-making, and structured financial planning. Addressing family financial problems early prevents escalation into severe debt stress.

Nidhi’s situation highlights the risks of ignoring oversight. Her family trusted her husband blindly. Open communication and clear boundaries would have spared them in advance. It’s essential for managing credit card debt and maintaining stability within the relationship.

What are the best debt management tips for couples?

Ans. Debt relief options include restructuring loans, negotiating settlements, and legally disputing fraudulent liabilities. In cases where debt was not a normal process, rather the debtor was a victim of malicious practices, the law always provides refuge to such victims.

In cases like Nidhi’s, forged signatures provide grounds for legal action, which may reduce enforceable debt. Her mother has been bedridden for years, so forging her signature is clearly visible here. Proper investigations can easily prove how it happened. They just have to take help from a good advisor. Exploring these options is critical for reducing debt stress and managing large-scale family financial problems effectively.

A Quiet Space to Think Clearly

When debt stress becomes overwhelming, it often brings confusion, fear, and emotional pressure that make decision-making difficult. Situations like Nidhi’s show how quickly financial stress in marriage can turn into a complex mix of emotional and financial challenges. Trying to handle everything alone can increase uncertainty and delay the right action.

If you are navigating similar credit card debt problems or struggling with dealing with financial stress, you may need a space where you can think clearly without judgment. Resource Owls offers a confidential Let’s Talk Session designed to help you reflect, organize your thoughts, and understand your situation with structure. This is not about giving you instant answers, but about helping you see your reality clearly so you can make better decisions. Sometimes, clarity is the first step toward solving even the most overwhelming problems.